Scams are becoming increasingly sophisticated and we thought it was time to update you on things to watch out for. There are three different scams that we will cover in this blog post. Please read and be aware.

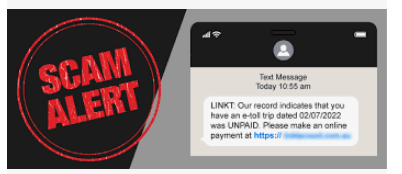

Text Toll Scams

I am a hyper-vigilant person when it comes to cyber security and scams, but I am also a very conscientious person. So on a Saturday morning a few weeks ago when I got a text telling me that I owed a toll, I was caught off guard and went to pay it. At the time I was thinking 'I'm sure I haven't driven anywhere where there is a toll, but I better pay the bill'.

The text was from a phone number, it wasn't claiming to be from Waka Kotahi or any other organisation. I was clearly caught off guard as when I realised it was a scam, I realise that it was an Australian phone number, and I hadn't driven anywhere in Australia for years (STUPID!)

I clicked on the link and put in my licence plate number and credit card. It said it would send me an SMS link to confirm, and when I didn't get the link I suddenly came to and realised it was a scam. Damn.

But, I thought I could deal with it as the card I put in had nearly expired and the new cards had just arrived, so I thought I could beat the scammers. I then spent the hours required changing the credit card to the new credit card, thinking I had saved myself.

Then a week later I heard from the bank (BNZ) saying that they had blocked both the old and new card (because the number was the same on both cards, it was just the CVC and the expiry date that was different), because there were unusual transactions. Cue a wasted 4 hours (well not wasted as it protected me, but I didn't have a spare 4 hours), talking to the bank, confirming which transactions were genuine, going into the bank to reset my access code, downloading the app again with the new code, waiting for the new cards to arrive (which amazingly arrived by courier within 24 hours), then going and reloading the totally new credit card details at all those sites again.

The scammers only got $2 off me, and the bank sorted that out. [This is the second time in 10 years that BNZ have picked this up for me, very impressed]. But I was luckier than the other 99,999 people. 100,000+ people have reported falling for this scam (and those are the ones that have reported it). Some people lost tens of thousands of dollars. Read more in the stuff article here https://www.stuff.co.nz/national/300898351/over-100000-reports-received-life-savings-lost-over-nzta-toll-scam

As a reminder, Stuff says: Advice for dealing with scams

Not all messages will look the same, as scammers change their wording over time.

Do not engage with or click any links before you know a message is genuine.

To check if a message is genuine, check directly with the people it came from. Go to the organisation’s website or check your online account directly.

Scam messages commonly contain bad or irregular spelling and grammar. Use this as your first sign that this could be a scam.

Never provide any card or personal details if you do click a bad link.

If you have paid money already, speak to your bank as soon as possible and let them know what’s happened.

It can be harder for people that don’t frequently use their phone to recognise a scam, such as the elderly or vulnerable. Check in with your whānau to help them learn how to avoid falling victim to an SMS scam.

13.50% for a term deposit with Yorkshire Building Society - $330,000 lost

This is a free to read article on the New Zealand Herald.

Comments from us on this scam:

a. Treat all Term Deposit comparison sites as dodgy apart from www.interest.co.nz.

b. If someone calls you with a 'special deal', 'offer that is only available for a short period of time' be suspicious.

c. Stick with the mainstream banks (that are listed on www.interest.co.nz) and stick with BBB plus rated banks from that site.

d. Ask yourself why an organisation wouldn't have a New Zealand bank account if they are offering investments in New Zealand?

e. Refer to www.interest.co.nz to see what a realistic term deposit rate would be. If it is not within the rates on that site, ask yourself what is happening.

f. If the bank questions you about your transfers, listen to them, they are asking you these questions for good reasons. They are trained to identify potentially risky transactions.

g. Here is a list of the registered banks in New Zealand, don't deal with any bank that doesn't have their own account to pay the money into.

7.60% for a term deposit with HSBC - $150,000 lost

This article on the NZ Herald is paywalled, so if you don't subscribe you won't be able to access it. We have summarised the points below.

This is another situation where someone was looking for a better deal on a term deposit comparison website, where the interest rate was higher than is currently being offered in New Zealand and where the bank account was not the bank account associated with the organisation that the money was being invested with.

Disappointingly, in this situation, the investor asked a financial adviser to 'run their eyes over it'. The adviser rang the number that had been given and felt that the person on the other end of the phone call 'seemed genuine'. (but then disclaimed that they weren't giving advice to the investor) This was also another situation where the bank that was transferring the money questioned the transaction.

Additional comments from us over and above the ones on the second scam above:

a. Don't trust a phone number that you have been given. Ring the listed generic phone number for the organisation that the investment is to be with and ask to speak with the person that has contacted you. If they are genuine they will work there.

b. Be suspicious if the organisation is a registered bank in New Zealand and doesn't have their own bank account for you to pay into. In this case it was an ASB bank account, for HSBC (which is a registered bank in New Zealand).

c. Be suspicious if you are offered a 'tiered' interest rate, higher return if you are investing more. There is nothing wrong with asking your bank to give you a higher rate because you have more, but the structure in this situation was unusual (usually you only get a small increase in interest). $100,000 for 24 months paid 7.6% interest, but $50,000 for 12 months only paid 6.2%.

d. Just because the organisation asks for Anti Money Laundering information and has a glossy brochure does not mean it is genuine.

Summary

Remember the old rule with the investment scams 'if it looks too good to be true it usually is.'

Update to this article on 16/06/2023. The Financial Markets Authority [FMA] today launched a notification to the public to be wary of the 'Compare Fixed Term Deposits (CFTD) - Comparison site is harvesting investor details to scam people.