Are you up-to-date with your FIF (Overseas Tax) obligations?

A recent article in the financial media highlighted the low compliance rate with the Foreign Investment Fund (FIF) rules, with a tax consultant suggesting that Inland Revenue (IRD) will likely catch up with those not declaring their FIF income.

The article points out the surprisingly low number of people who declared FIF income in recent years, suggesting a significant degree of non-compliance.

What is FIF and why is it important?

In essence, the FIF rules are a way for New Zealand to tax the income earned on overseas investments. If you hold overseas investments and are a New Zealand tax resident, you are most likely subject to FIF rules, unless you meet certain exemptions.

The most common exemption is if you own less than $50,000 of these investments per person (at cost price). If you have an investment portfolio, your investment platform will work out the tax for you. For Moneyworks clients, we have already alerted you in late 2024 about this IRD programme. If you invest through an entity (like a Family Trust or a Company) you will automatically be subject to the FIF rules.

Interestingly, over the years, we have found the tax calculation to be relatively favourable to our clients, but there are also more PIE (NZD and Tax Based) investments available, which reduce the tax liability for our clients.

The rules can be complex, with up to five different calculation methods depending on the type of investment and how you are investing. The IRD has published an interpretation statement to help taxpayers understand the cost method, which is generally used for unlisted investments.

What happens if you don't comply?

Failing to disclose FIF income can lead to penalties from the IRD. It's better to voluntarily disclose any undeclared income than to wait for IRD to find it.

The IRD is now actively cross-checking income tax returns with data received under the Common Reporting Standard (CRS), making it more likely that non-compliance will be detected.

What should you do?

● Check if you need to file a FIF tax return. If you are unsure whether you need to file a FIF return, you should contact your financial adviser, accountant or the IRD directly.

● Understand your obligations. The FIF rules can be complex, so it's essential to understand your obligations. You can find more information on the IRD website or by talking to a tax professional.

● Keep accurate records. Make sure you keep accurate records of your overseas investments and income. This will make it easier to calculate your FIF income and file your tax return. If you have an investment portfolio, the options available will be calculated for you, and the guide form the platform should show you how to plug the information into your tax return.

● Claim your expenses. Remember that you can claim expenses related to your overseas investments against your FIF taxable income. This includes things like investment management fees.

● NOTE - you are unlikely to be fulfilling your obligations if you are just doing an online tax returns, unless you have filled in the separate FIF obligations information.

Don't wait for the IRD to catch up with you. Take steps to ensure you're meeting your FIF obligations and contact IR directly through the secure mail on your IR login, or by calling them (for non-businesses they seem to have quite a quick answer time period). Check if you need to adjust your returns for previous years as well.

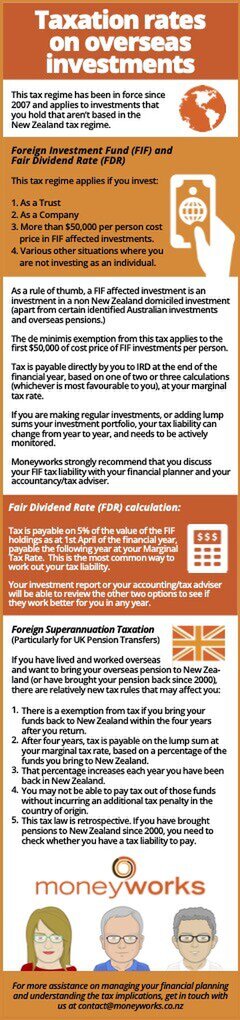

The infographic below is from May 2017 - but still applies - check it out for more details.