Part of the volatility on international financial markets since the start of 2016 has been related to the concern about the highly leveraged European banks and whether they will be able to pay the interest on the CoCo’s (Contingent Convertible bonds) that they have issued. See Bernard Hickeys excellent summary of the issue here.

A major concern was whether Deutsche Bank would default on its liabilities. As of yesterday, a number of banks have reassured investors that they can easily pay their bills, the prices of CoCo’s (which have been heavily purchased by investors) has fallen dramatically.

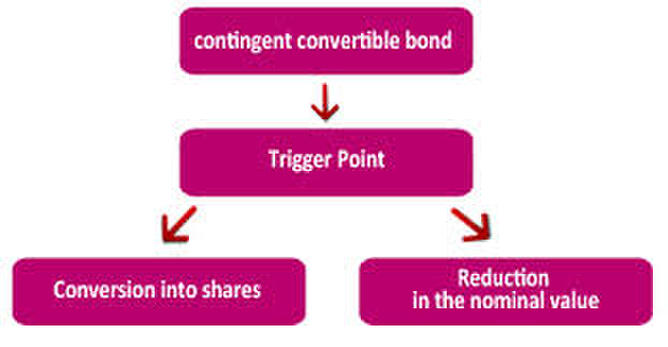

CoCo’s are ‘designed to make banks safer’, but mean that banks can stop paying the interest coupon when profits evaporate. If the bank gets into trouble – the debt turns into equity (see Financial Times summary in Bernard Hickeys note above). See this summary by the Telegraph.

As the Financial Times stated:

Cocos are the riskiest debt issued by banks, with only a quarter of the eurozone market judged investment-grade by credit rating agency Fitch last year. Retail investors are not supposed to be involved in the €95bn market where coupons are high — frequently 6-7 per cent, compared with below 1 per cent for senior bank debt — to compensate for the risk of loss-absorption, and the risk that payments will be halted.

New Zealand investors are highly unlikely to be invested directly into CoCo’s, but if you hold International Fixed Interest investments in your portfolio, your fund manager may have an investment in these. Moneyworks clients currently have NO International Fixed Interest Investments in their portfolios.

However, this raises the question of whether there are any investments like the CoCo’s in New Zealand.

Fortunately, Gareth Vaughan at interest.co.nz has done the research and discovered some Fixed Interest issues with similar characteristics. Read his commentary here.

What are the New Zealand investments with similar key features?

As Gareth Vaughan notes, here have been $1 billion of securities with the same features as CoCo’s issued, and the FMA issued a warning to investors in 2015 that these investments may not be suitable for many investors.

The FMA points out common features of these bank securities include; The bank may stop interest payments, or reduce the amount of interest they pay to investors, even if they’re still in business. The bank can convert the notes into shares in the bank, or its parent company, and the value of those shares at the time they are converted may be a lot less than the amount paid for the capital notes. Additionally, the notes may be cancelled so investors lose some or all of their investment, even if the bank is still in business. And decisions on buy-backs are usually the bank’s call to make.

The investments that fall into this category are noted below, with some additional commentary from Gareth Vaughan:

ANZ, ASB & Kiwibank (Thanks to www.interest.co.nz)

New Zealand bank securities of this ilk include; a $400 million issue of subordinated and unsecured debt securities by ASB in April 2014, a $500 million issue of convertible notes by ANZ NZ in March 2015, a $150 million 10-year subordinated bond issue by Kiwibank in December 2012, and a $100 million 10-year Kiwibank capital notes issue in June 2014.

No other New Zealand banks have issued this type of security to the public to date. However, TSB Bank deputy CEO Charles Duke told me last year a new TSB ownership structure was partly designed to enable it to issue hybrid capital instruments. Duke did say, however, there were no imminent plans to issue such securities and TSB hasn't done so to date.

Heartland Bank has disclosed plans for a debt securities issue of between $50 million and $75 million that may include the features outlined above.

The ANZ "mandatorily, convertible, non-cumulative perpetual subordinated notes" are listed on the NZX debt market. Paying a 7.2% annual interest rate, they were trading at a 4.75% premium as of Thursday. They have no fixed maturity date with the current interest rate set until May 2020.

The ANZ notes have a BBB- credit rating from Standard & Poor's, the lowest investment grade rating, versus ANZ's own AA- S&P rating. See credit ratings explained here.

The subordinated and unsecured ASB debt securities, issued for 10-years but with a five-year call date, are paying 6.65% per annum. Also listed on the NZX debt market, they are trading at a premium of 6.68% at the time of writing. They have a BBB+ S&P credit rating versus ASB's AA-.

The two Kiwibank issues both have BB+ credit ratings, S&P's highest speculative, or "junk," rating. Kiwibank itself has an A+ rating. The 10-year subordinated bonds issued in 2012 have a call date in December 2017. They're paying 7.25% and are trading at a 6.5% premium. Kiwibank's 2014 capital notes, which have a call date in July 2019, are paying 6.61% and trading at a 5.8% premium.

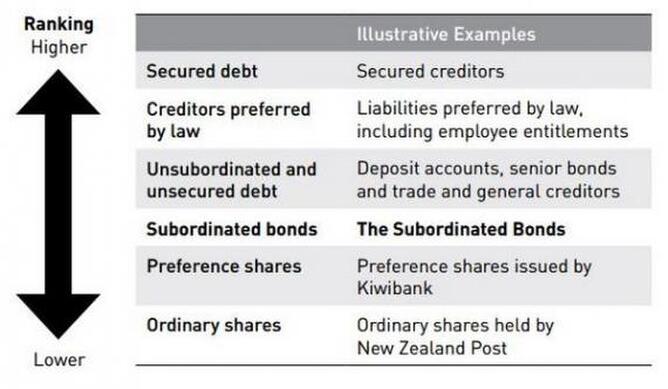

The table below shows how the Kiwibank subordinated bondholders would be placed in a liquidation.

Summary

As outlined above for the Southern Cross Finance Contributory Mortgages and in the article about managing your retirement investments, Moneyworks do not recommend that you invest in these higher risk investments unless you fully understand the risks involved.

Even if you do understand the risks involved, it is vital that you weigh up whether you are going to get additional return for the much higher risk, and whether you might be better diversifying your portfolio and adding some equities and listed property investments.

If you would like to discuss the options of creating a well diversified portfolio and a plan for managing your retirement capital with one of Moneyworks Financial Planners, contact us by clicking here.

If you have any thoughts or opinions that you would like to share, visit us at our Twitter, Facebook or Linked In pages, and comment.

For more blog entries that you might be interested in:

How safe are your New Zealand Term Deposits?

How to get the most out of your term deposits

Are investors getting too greedy with fixed interest again?

What are Fixed Interest Investments in New Zealand?

Fixed Interest Secondary Market – a what????

By Carey Church