This is relevant to you if you are a Trustee or Beneficiary of a Trust, have considered having a Trust, or know someone who is a Trustee of a Trust.

In 2016, I studied the third year compulsory law paper ‘Equity and Succession’. As well as covering the different issues with wills, we studied the detail of the various types of trusts – express/discretionary trusts, resulting trusts, constructive and charitable trusts.

From the creation of trusts in the Commonwealth legal system in the 14th and 15th centuries, to enable assets to be managed in the absence of the settlor, they have become a core part of society. Trusts play a central role in New Zealand society and are used in many sectors of our society and economy, including to hold wealth.

The existing legislative framework is made up of the Trustee Act 1956, multiple sources of case law on different topics and a number of other Acts that are relevant.

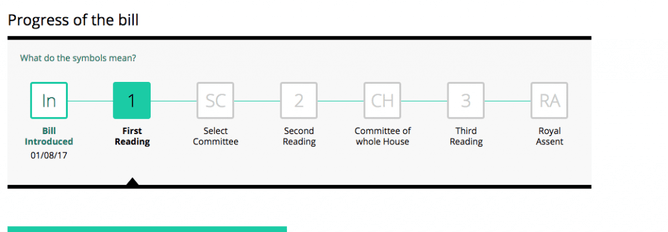

After many years work by the Law Commission, since November 2010, the Trusts Bill is currently before Parliament, and will bring a lot of the trust law into one place and make the law more accessible, although case law is still relevant.

The Bill aims to make trust law easier to administer, by setting out the core principles, including:

- essential features

- mandatory and default trustee duties

- requirements for record keeping

- rights of beneficiaries to information

We recommend that every Trustee take the time to understand the legislation. Trustees will have 18 months to ensure that they comply with the new provisions, which will apply to existing and future Trusts.

We work with Moneyworks clients to remind them regularly of their responsibilities as Trustees (which requires a different hat to be worn than when they are a beneficiary), and to make sure that all the relevant documentation is completed and up to date.

It is important to remember that any assets that you transfer to a Trust are no longer yours, they belong to the Trust, and have to be managed for all beneficiaries, and not for you personally.

While a number of people have put in place Trusts in the last 20 years, we are not sure that a Trust adds value to all of our clients lives. If you have a Trust in place, we recommend that you use the introduction of this new legislation to review the following:

Why do you have a Trust in place?

- Do you keep all of your paperwork and documentation up to date and review it regularly?

- Do you always act consider all beneficiaries?

- Do you always act in accordance with the Trust Deed and your legal requirements?

- Should you continue to have a Trust? What are the advantages to you for doing this?

- If you retain a trust, will you outsource some of the management and record keeping, or manage it yourself?

We recommend that you take time to consider the role of your Trust, and seek external advice as to whether there is any value in retaining your Trust. The historic protections against asset and means testing, beneficial tax rates and other benefits no longer exist. From a financial planning perspective, clients having a trust in place can cause complications and administrative costs that outweigh any benefits from retaining a trust.

If you have any thoughts or opinions that you would like to share, visit us at our Twitter, Facebook or Linked In pages, and comment.

For more blog entries that you might be interested in: