Banks being held responsible for fees, conduct and lending practices

Our banks are an integral part of our lives and pretty much hold us hostage with their fees and decisions, unless we choose to be part of the barter economy, or become self sufficient, we will always have to have an involvement with banks.

Over the last year we have seen banks phase out cheques, close more branches, limit branch hours and replace humans with chatbots on line. While we are active users of technology to make everyones lives more streamlined, some of these changes from the banks have disadvantaged more vulnerable people and people who choose not to participate in the technological world, for many reasons, including concern for the security and safety of their information and money.

Some bank practices are now being questioned and challenged with the new Conduct of Financial Institutions (COFI) Bill going through parliament, which will require financial institutions to put in place conduct policies and processes that are in the interest of the customer (and not just the shareholder).

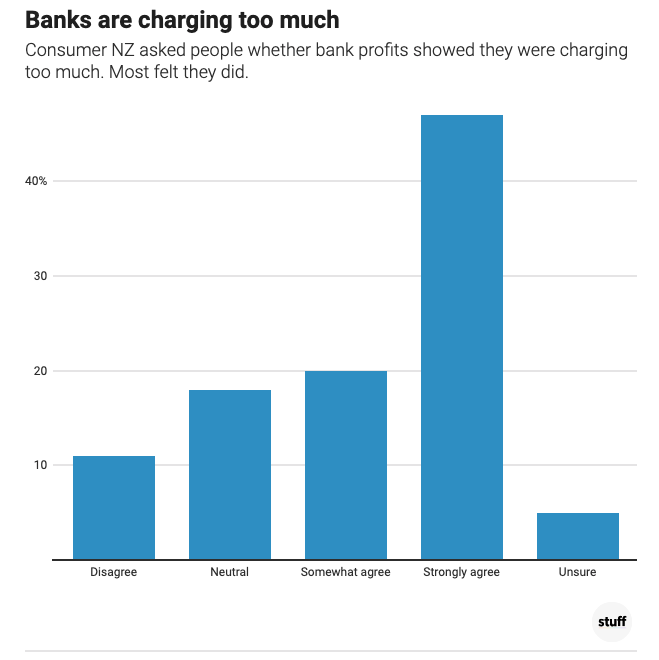

Some changes are happening in advance, these are outlined in this article from Rob Stock, which I suggest that you skim read at least, to understand what is happening. It is good to see some changes happening (particularly when you look at the graph attached to this post - thanks to Stuff), showing that most people agree or strongly agree that Bank profits showed that banks were charging too much.

As Rob Stock outlines, complaints to the Banking Ombudsman, and the Financial Markets Authority has lead to compensation for clients who had been treated unfairly - here are some examples from the article:

Banks’ past failures to adhere to lending laws have resulted in a lot of compensation payments for companies. ASB has had to fork out $9 million this year for past responsible lending law breaches, and $8.9m for historic overcharging on home loan break fees. Last year, ANZ had to stump up $29.4m for responsible lending law breaches dating back to 2015.

Gaping hole in the banking regulation net about to be closed