That was the title of an email that I received from a client recently, referring to the latest fall in the sharemarkets. They are correct, it is a sea of red, but there are some really important things to understand.

Market Cycles

Markets (actually pretty much everything in the world) move in cycles. It is generally thought that the financial markets move in a 7 year cycle, with expectations that they will 'correct' every 7 years. The last time we had a major correction was in the Global Financial Crisis from 2008 - 2010. We are long overdue for a cyclical correction. We thought that the arrival of Covid in March 2020 was heralding the long overdue correction, but the markets bounced back up and kept on rising.

Therefore, it is not unexpected that the markets are correcting and in fact it is healthy.

Why are the markets correcting?

The reasons for the corrections are a surprise for many people, the rate of inflation and the reaction of the central banks in increasing interest rates to try and limit the rate of inflation. As you will know, this is combined with the Russian invasion of Ukraine.

This has exacerbated inflation with issues around the supply of energy and food crops, which has combined with the supply chain delays (and therefore supply not meeting demand and traditional economic scenario for increasing prices) and (according to many commentators) the increase in prices because of the 'flushing of cash' from central banks keeping economies going (particularly over the last few years).

Changes in desirable investments

A number of commentators believe that this market correction will also involve a change in the types of companies that will lead the next bull markets. The technology companies have led the last bull market (particularly in the latter phases) and many are now facing a number of logistical and regulatory challenges (like privacy laws, use of content laws, competition - see Netflix). Some technology companies are likely to be leaders in addressing these issues and continue to be great companies for investing, while others will wilt under the winds of change. It is up to your fund managers to make those calls (and up to us as your advisers to take this information into account when making recommendations in your portfolio).

It is suggested that new areas of desirable investments may include renewable energy and sustainable businesses taking advantage of the circular economy.

What does this mean for you?

It is important to understand that a sea of red is not a good reason to change your long term investing strategy. If you withdraw your investments now, or change your risk profile now, you are locking in any losses. However, you can move your investments around, as long as they are moved in the same market (ie over a few days), as long as you aren't doing this as a knee-jerk reaction.

Markets DO go back up again and when they do, they go up quickly with no notice.

Refer to the graphs above and below.

The graph above is the indicator index the S&P500 over the last year. As you can see the markets (as represented by the largest 500 US companies) peaked on the 29/12/2021. The first low in this bear market was on 16/06/2022 and then the markets bounced back quickly to the next peak on 15/08/2022. The news was not getting any better, so they have gone down again. It may be that the 12/10/2022 was the low for the entire bear market, it may be that it is still coming.

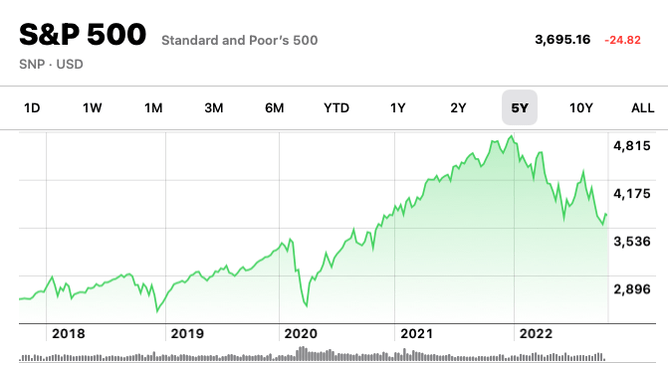

Then look at the 'sea of green' pictures beneath this blog article. These show the S&P over 2 years, and you can see that the markets now are only back at where they were in December 2020. (That doesn't help if you have invested your money or started investing since then, we know, but remember these are long term investments).

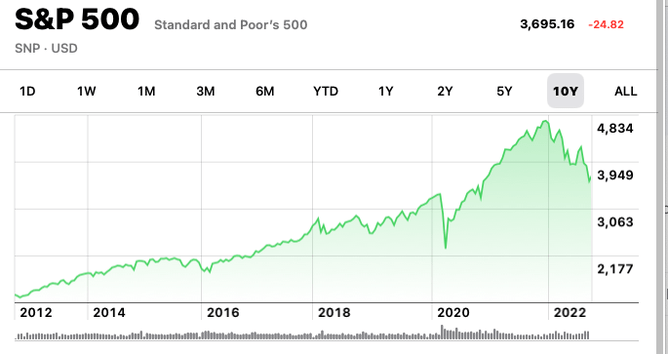

The next graph shows the S&P over 5 years, follows by the 10 year graph and then 'All Time' which illustrates that markets do go up (and quickly) after they have fallen.

But the important thing to understand is that when markets go up, they do so quickly (with not enough time for you to get into them - and you won't be sure whether it is a false bounce like we saw in August). It is important that you leave your long term money invested where it is, and always make sure that you have short term funds in cash if you are reliant on your investments to live off.

Check out the articles in our blogs on why investors do what they do to understand why we want you to just sit tight.

If you have any questions or want to talk about this, don't hesitate to contact your adviser.